Bitcoin on-chain analysis, an overview of 7/22/22–7/29/22

Bitcoin On-Chain and Derivatives

Markets have rallied after the Fed has announced they’ve raised rates another 75BPS, with Bitcoin leading the charge up 15% from its lows this week.

An important weekly level for BTC to reclaim is its 200-week moving average, currently at $22,800.

Monthly also appears to be reclaiming its 180-week EHMA, a level we’ve talked about over the last few months as a macro accumulation area for BTC.

Have been watching, is the market capitalization of USDC and USDT relative to the aggregated crypto market cap.

Whenever this ratio reaches the bottom of its channel, it indicates that there is a small amount of dry powder relative to what has already been deployed, increasing the likelihood of a macro top as there are minimal new buyers.

Conversely, whenever the ratio reaches the top of the channel, it indicates that there is a large amount of dry powder on the sideline relative to crypto’s aggregated market cap.

As the market rallies, there is a more substantial likelihood of market participants becoming induced to chase.

The more dry powder the more dry kindle there is for a spark to light on fire.

Comparing stablecoin’s market cap to solely BTC’s market cap and then adding Bollinger bands.

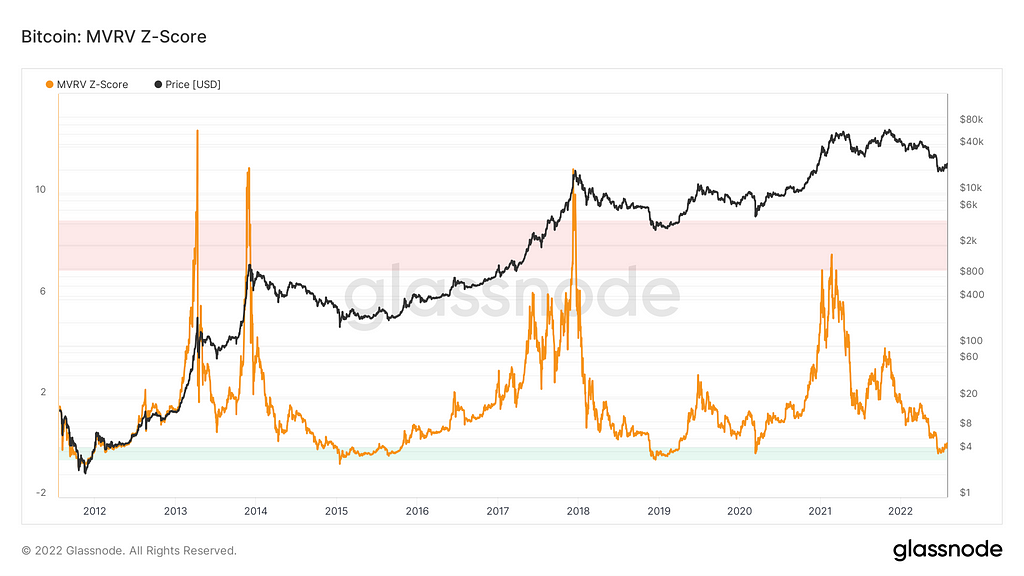

MVRV z-score was another indication we’ve been watching for since late last year as an area of interest for long-term spot buys.

After spending about a month below, the ratio has begun to peek out of its accumulation zone.

It has now reverted back, no longer at that level of extreme deviation that has market historical bottoms.

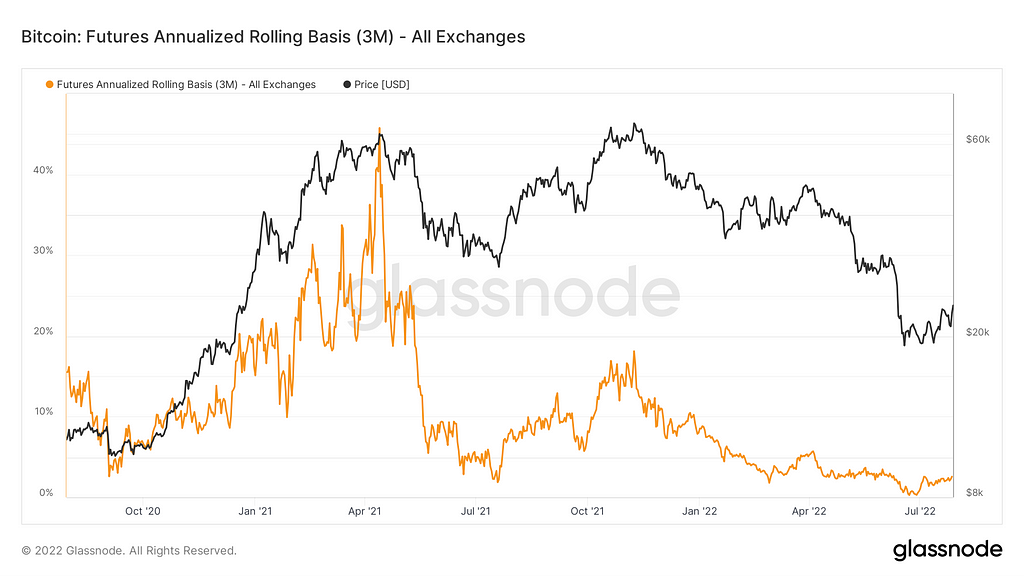

Bitcoin’s 3-month basis has recovered slightly from 0.27% and even backwardation on some exchanges last month, to 2.57%.

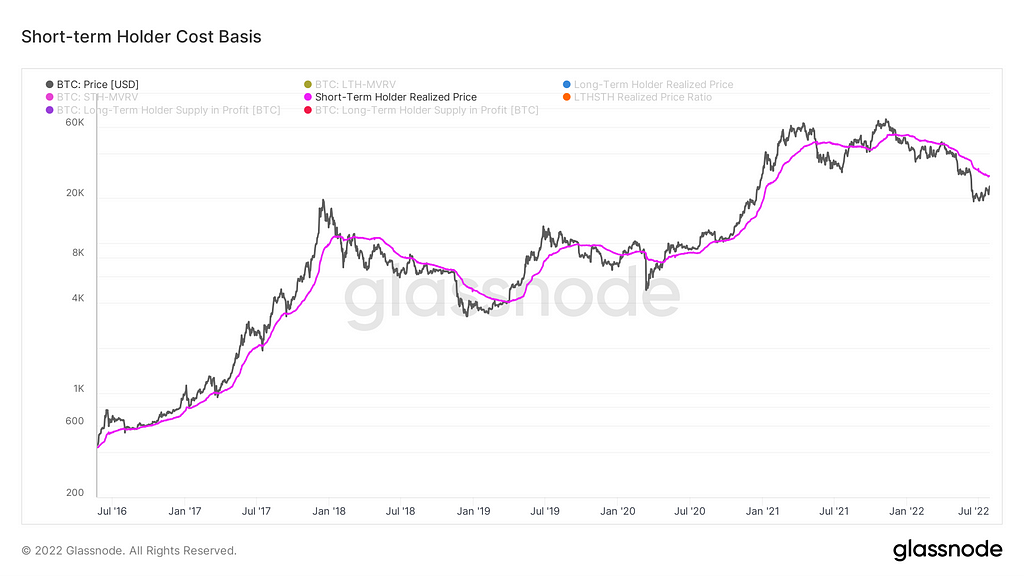

In terms of items we still want to watch out for on the Bitcoin-native side, the short-term holder cost basis is an important threshold to keep in mind that we’ve discussed for a year plus.

This is the aggregated cost basis of short-term holders (<155 days).

Currently sitting at $28K, is the confluence with technical resistance as an area of confirmation for momentum-based market participants.

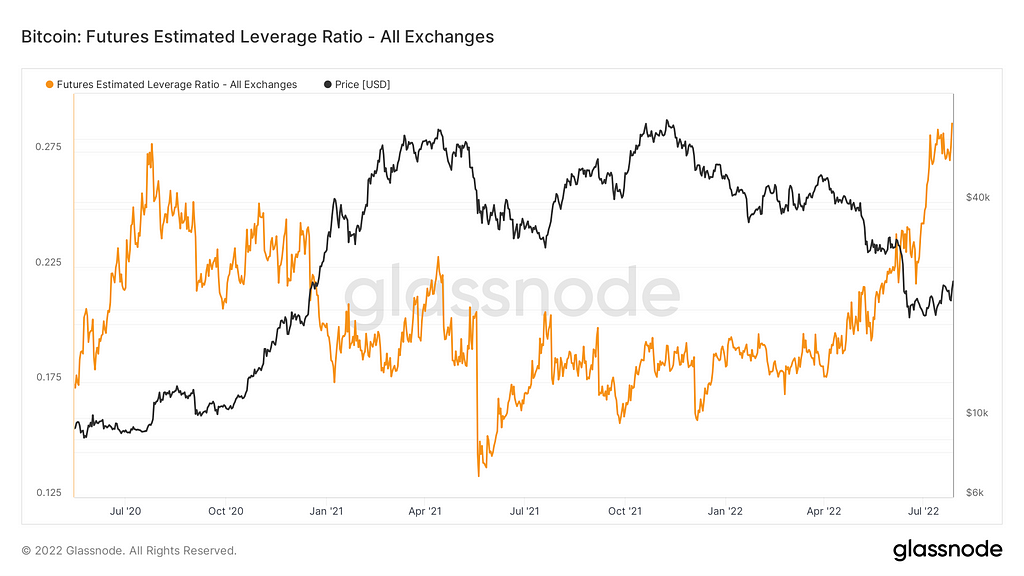

Funding is relatively muted so nothing of major concern, but what we really want to see for high conviction reversal is the funding going further negative as BTC grinds upwards.

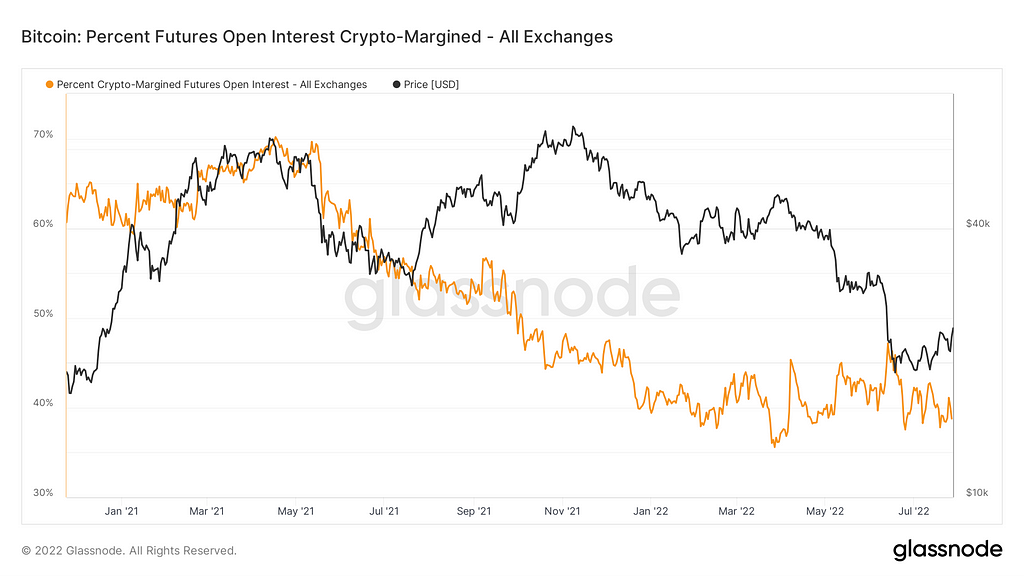

This compares Bitcoin’s open interest to the number of BTC on exchanges as a proxy for leverage in the system.

New to trading? Try crypto trading bots or copy trading

Bitcoin on-chain analysis, an overview of 7/22/22–7/29/22 was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.