Telegram is a feature-rich messaging alternative to WhatsApp

Telegram lets you create group chats with up to 200k members, share media files up to 2GB each, and all your messages are stored in the cloud, so you can easily access them from anywhere.

Computers Tech Games Crypto Music and More

The OneXPlayer Mini AMD is a handheld gaming PC that boasts many great qualities, making it a worthy challenger to the Steam Deck and other portable competitors. While each device has their own unique set of strengths and features, one key advantage this orange-black pocket rocket has over Valve’s portable powerhouse could tip the scales in its favour.

RELATED LINKS: Best SSD for gaming, How to build a gaming PC, Best gaming CPU

Many types of loans are available to consumers. It can be confusing to know which option is best for you. In this blog post, we will discuss amortized and interest-only payment schedules, and the benefits of each. We’ll also explore alternative mortgage loan options. So, whether you are looking to buy a home, refinance your current mortgage, or just get a better understanding of the types of loans out there, read on for information on the different types of loans available to you.

A fixed-rate mortgage has a set interest rate that does not change for the life of the loan. This type of mortgage is ideal for those who want predictability and stability in their monthly payments.

An adjustable-rate mortgage (ARM) has an interest rate that can change at any time, based on the current market conditions. This type of mortgage is ideal for those who are comfortable with some risk and want to take advantage of potential savings if interest rates go down.

There are also several subtypes of ARMs, including:

An amortized loan is a type of mortgage in which the principal and interest are repaid over a fixed period of time. This repayment schedule is determined when you take out the loan, and it cannot be changed. The amortization period typically lasts between 15 and 30 years, but it varies depending on the lender. During this time, your monthly payment will remain constant, even if the interest rate changes. This makes amortized loans a good choice for borrowers who want predictable monthly payments.

Interest-only payment schedules are becoming increasingly popular among homeowners. With this type of loan, you only pay interest on the outstanding balance of your mortgage each month. The principle remains unchanged, so your total payments will be lower than if you had an amortized loan. However, your total interest payments will be higher, and the principal balance of your mortgage will increase over time.

With this type of payment schedule, you can keep your monthly payments low. It can be helpful for those who are expecting a large expense in the near future, as it gives them more breathing room in their monthly budget. It is also a solid option for those who have plans to move or refinance within a few years.

FHA loans are mortgages that are backed by the Federal Housing Administration (FHA). This means that the government guarantees that FHA-approved lenders will be repaid if you default on your loan.

Because of this guarantee, FHA loans are often easier to qualify for than other types of mortgages. In addition, FHA loans come with a variety of features, including:

VA loans are mortgages that are backed by the Department of Veterans Affairs (VA). This means that the government guarantees that VA-approved lenders will be repaid if you default on your loan.

VA loans come with a variety of features, including:

USDA Rural Development Loans are mortgages that are backed by the United States Department of Agriculture (USDA). This means that the government guarantees that USDA-approved lenders will be repaid if you default on your loan.

USDA Rural Development Loans come with a variety of features, including:

Conventional loans are mortgages that are not backed by the federal government. This means that there is no guarantee from the government that these lenders will be repaid if you default on your loan. However, this also means that conventional loans typically have lower interest rates and more flexible terms than other types of mortgages.

When it comes to conventional loans, there are two types: fixed-rate and adjustable-rate. With a fixed-rate loan, your interest rate will stay the same for the entire duration of your loan. This can be helpful for those who want predictability in their monthly payments. With an adjustable-rate loan, your interest rate can change throughout the life of the loan. Aside from a traditional mortgage, here are additional loans available to you:

A home equity loan is a type of loan that uses the equity in your home as collateral. This means that you are borrowing against the value of your home to get money for other purposes, such as home improvements or debt consolidation.

One thing to note about home equity loans is that they typically come with higher interest rates than other types of loans. However, this may be worth it if you can get a lower interest rate on your credit card or other debts.

A personal loan is a type of unsecured loan that can be used for any purpose. This means that you do not have to use the money for something specific, like buying a car or refinancing your mortgage.

Personal loans typically come with lower interest rates than credit cards, but they also have shorter terms. This means that you will need to pay back the loan in a shorter amount of time.

Refinancing is the process of taking out a new loan to pay off an existing loan. This can be helpful if you are able to get a lower interest rate on your new loan, as it means that more of your monthly payment will go toward paying down the principal balance instead of going toward paying interest charges.

Bridge loans are a type of short-term loan that can be used to cover the gap between the purchase of a new home and the sale of your old home. This can be helpful if you need money to move before your old home is sold. Bridge loans typically have high-interest rates, but they can help you get into your new home sooner.

A cash-out refinance loan is a type of refinancing that allows you to get extra money from your home equity. With this type of loan, you can pay off your old mortgage and take out additional funds at the same time. This can be helpful if you need money for things like home improvements or debt consolidation.

A reverse mortgage is a type of loan that allows homeowners aged 62 and older to convert the equity in their home into cash. Homeowners can use this cash for things like paying off their current mortgage, making repairs on their home, or covering medical expenses.

A direct lender is a company that offers loans directly to consumers. This means that you can apply for the loan at their website or office and get approved without having to go through another company.

A mortgage broker is a company that helps you find the best mortgage for your needs. They work with a variety of different lenders, and they can help you get approved for a loan even if you have bad credit or are self-employed. Some popular mortgage brokers include most banks, credit unions, Fannie Mae, and Freddie Mac.

A correspondent lender is a company that originates loans but then sells them to another business. This can be helpful if you are looking for a specific type of loan or want to work with a certain lender. Some examples of popular correspondent lenders include the FHA, the VA, and the USDA.

When it comes to choosing a loan, it is important to consider your needs and goals. Do you want a low monthly payment? Or are you more interested in locking in a fixed interest rate?

Also, think about how long you plan on staying in your home. If you think you will sell or refinance within the next few years, an adjustable-rate mortgage may be a good option for you. However, if you plan on living in your home for many years, a fixed-rate mortgage may be the better choice. There are many different options available and the one you choose depends on your goal.

New to trading? Try crypto trading bots or copy trading

Types of Loans & Alternative Mortgage Loan Options was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.

With waiting lists and frustrating delays in the NHS, new alternatives are rising on the market. Welzo is an ambitious…

The post The Healthcare System Needs a Modern Alternative – Meet Welzo appeared first on TechRound.

So far, Cosmos’ IBC seems to have stayed clear of troubled waters.

Got this unique app idea nobody has come up with before? Or maybe there’s a glaring niche in your region for a traditional payments or delivery app so popular elsewhere in the world? More and more tech entrepreneurs become aware that choosing to develop these on blockchain, instead of traditional web2 networks, bears numerous technological advantages.

But not all of them are aware that besides decentralization, immutability and transparency, opting for web3 tech might also get an easier access to funding. A single letter in your business plan may not only make VCs start paying attention, but also open the web3 gates to the whole new ecosystem of funding sources.

Traditional private investment vehicles will probably remain for some time the main means of attracting large cash flows for fintech start-ups, and we’ll get back to these in a minute. But first let’s look into funding alternatives the thriving blockchain industry has to offer. This will help you decide whether it is an app or a dapp that is most suitable for your next venture.

From ICOs to Developer Grants — Web3 is Rapidly Changing Tech Fundraising Landscape

Despite it’s no longer 2017, ICOs, Token Generation Events or Pre-sales remain a major instrument for attracting initial funding in the cryptoverse. However, there are already around 10,000 tokens in this market, meaning the competition is overwhelming. At the same time, retail investors’ appetite has fallen sharply due to countless scams and the general market correction.

Besides, issuing crypto tokens and relying on retail investors isn’t something that necessarily suits every business model or digital product. In that case a good bet is to pick a thriving blockchain ecosystem, and apply for some of the increasingly popular developer grants. This way you not only get to create on a technically superior decentralized network — you are also paid to do that.

The DFINITY Developer Grant Program is one good example of such an alternative web3 financial resource supporting both the growth of the Internet Computer ecosystem and start-ups working in it. Funding from $5,000 to $100,000 is offered to developers and teams creating dapps and other decentralized tools and catalyzing growth of the ICP blockchain. A total of CHF 200 million is allocated to that end. There are already 264 dapps running on this network, and DFINITY Foundation itself has 250 developers dedicated to improving the blockchain.

Developer Grant Program, however, is not meant to be a source of venture funding. If you are actively fundraising, dedicated funds like Beacon Fund managed by Polychain Capital is most likely a better fit for your venture.

Number of Fintech Start-Ups is Going Ballistic, 90% of them fail

According to Boston Consulting Group, the number of fintech startups worldwide tripled in the last two years, rising from 12,200 in 2019 to 26,000 in 2021. And it is mainly blockchain tech that accelerates this revolution. Besides fintech, blockchain and a wider distributed ledger technology revolutionizes dozens of different industries like logistics and supply chain management, healthcare, cybersecurity, entertainment and others.

In the highly competitive tech world, attracting sufficient funds in time and being able to scale your operations is a prerequisite for success. And fundraising in 2022 isn’t getting easier, especially bearing in mind the grim macro outlook we are currently faced with. It’s no coincidence that 90% of all start-ups fail, and 82% of these — due to cashflow issues.

Now creating your product on blockchain purely for easier funding or better marketing most likely won’t work for obvious reasons. Instead, consider building on blockchain if your product would benefit from data security, transparency, trust without intermediaries or decentralization.

In this case, tapping into advantages of DLT organically might provide you with a crucial bonus of getting a quicker access to a longer runway. And experienced entrepreneurs know all too well an extra mile in the runway might mean the difference between Radio Shack and Spotify.

Blockchain Is the New Website for Private Investors

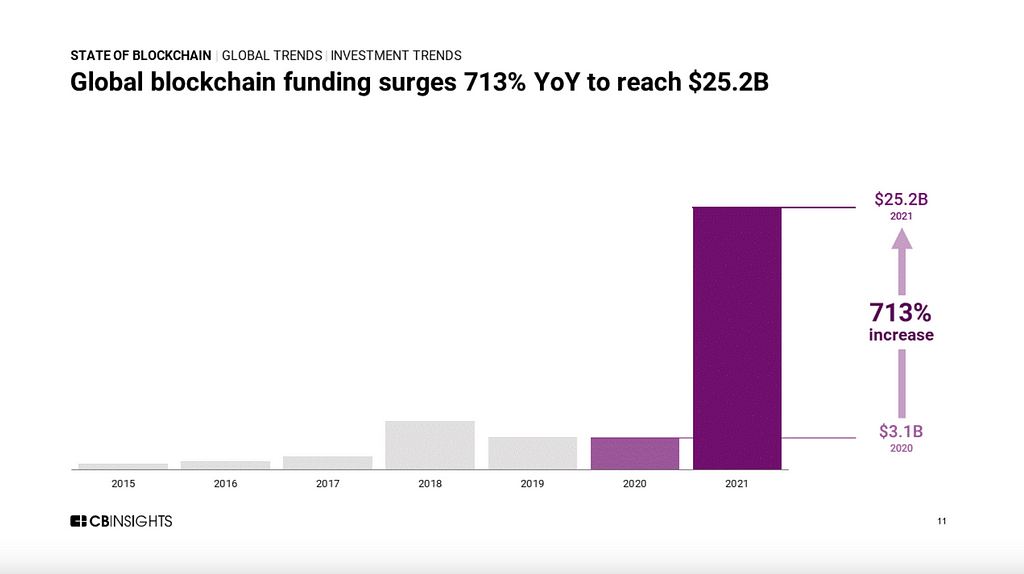

According to CB Insights’ “State Of Blockchain 2021” report, more than $25 billion worth of venture-capital funding went to blockchain startups in 2021, demonstrating a sevenfold increase from $3.1 billion in 2020. American start-ups alone attracted $6.26 billion with 157 deals. Increasing institutional and consumer demand for crypto-related products and services were identified as leading factors behind this gargantuan growth.

So this exponential growth paired with general trends in the market hints fundraising entrepreneurs at an obvious choice. In a hypothetical situation where potential investors are pitched with two otherwise identical products, they’d be more likely to choose the one with organically integrated blockchain features.

The current situation could even be compared to the Dot.com bubble in a sense. Somewhat anecdotical stories used to go about in the business community at the time. Entrepreneurs recounted numerous situations when banks and investment funds were more interested in the website than in one’s business plan.

Explosive Mix Fuelling a Decade-Long Run

· Urgent need to fundamentally improve web2-based legacy systems

· Rapid development of dozens of technologically superior DLTs

· Shortage of engineers able to develop on web3

· Willingness of VC funds to capitalize on the shifting web paradigm

– all these blend perfectly into an explosive mix. The mix that will fuel for years the businesses and professionals able to capitalize on it, but could bear extensive opportunity costs on the ones ignoring it.

And in case you are wondering if it’s not too late to capitalize on this growth, here are two more facts to wrap it up:

· There are currently 27 million active developers in the world, but only 18 thousand of them are developing web3 applications.

· Already exponential web3 growth is estimated to continue at least till the end of the decade.

Join Coinmonks Telegram Channel and Youtube Channel learn about crypto trading and investing

Not Only Tech: Web3 is Opening the Floodgates to Alternative Funding Sources was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.