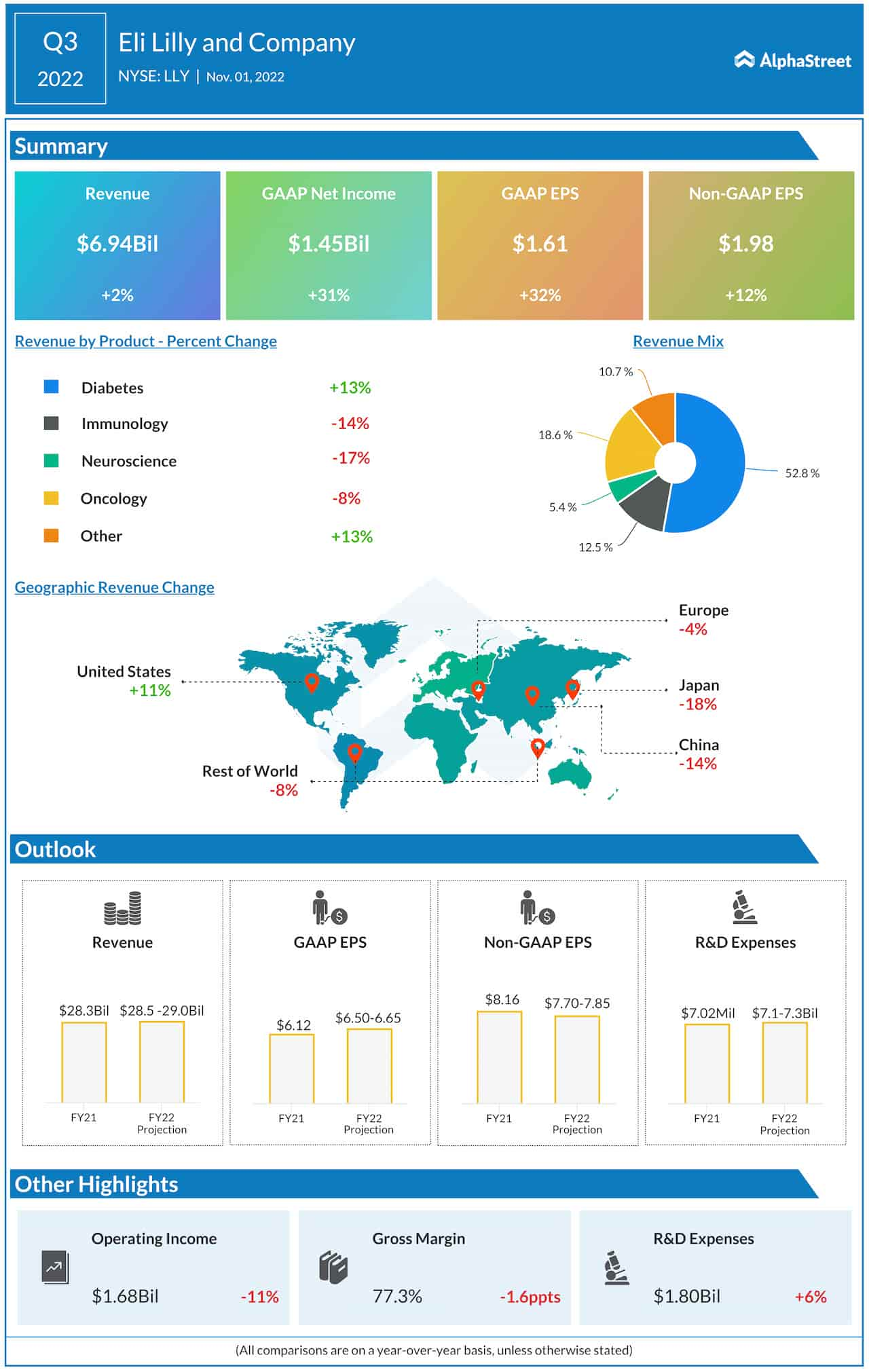

The global oil and gas industry generated record free cash flows last year of over $1.4trn, putting BP (LSE:BP) shares on many investors’ radars.

I’m bullish on fossil fuels in the medium term, and I wouldn’t shy away from adding an oil and gas giant to my portfolio.

However, I found some red flags in BP’s cash flow statement.

Windfall of war (and underinvestment)

BP’s operating cash flow – revenue minus operating expenses – soared from $12.2bn in 2020 to $40.9bn in 2022.

| Operating cash flow ($ million) | |

| 2020 | 12,162 |

| 2021 | 23,612 |

| 2022 | 40,932 |

US President Joe Biden said in October last year: “Oil companies’ record profits today are…a windfall from the brutal conflict that’s ravaging Ukraine...”

But President Biden left out an important factor: oil and gas prices have also risen because of underinvestment in the sector strangling production.

With politicians around the world banging the drum for a fossil-fuel phaseout, capital-intensive and multi-decade exploration and extraction projects look even riskier than normal.

Still, I believe oil will continue being the life blood of the global economy for decades. Materially intensive ‘green’ technologies are non-existent or in an embryonic stage throughout most of the developing world.

Therefore, I want to own shares in an oil and gas company that has the foresight to keep diligently investing in the future of fossil fuels.

I just don’t believe BP fits the bill.

Cash flow cannibal

BP’s operating cash flow increased by 237% from 2020 to 2022. Meanwhile, the company’s outgoings on financing new projects increased by only 75%.

While $27.3trn on financing activities between 2020 to 2022 sounds like a lot, consider that the company divested $17.3trn of its assets over the same period, for a net figure of just $10trn.

| Net cash used in financing activities ($ million) | |

| 2020 | (7858) |

| 2021 | (5694) |

| 2022 | (13,713) |

Now, compare that with how much the company paid out in dividends and share buybacks, elements included in ‘net cash used in financing activities’.

| Net cash provided by (used in) financing activities ($ million) | |

| 2020 | 3,956 |

| 2021 | (18,079) |

| 2022 | (28,021) |

Of course, everyone likes dividends and share buybacks. But when overdone, these feel-good activities cannibalise a company.

There is also an element of glass and mirrors here. That’s because, despite the hullabaloo about BP’s mammoth share buybacks, the company simultaneously expanded the number of outstanding options, through equity-settled employee share option plans, by 1,900% between 2020 to 2022.

| Number of options outstanding (millions) | Weighted average exercise price ($) | |

| 2020 | 28.2 | 3.79 |

| 2021 | 590.9 | 4.26 |

| 2022 | 564.1 | 4 |

This implies a dilution that will, to some degree, undo the share buybacks.

Having drilled into BP’s financials, I’ve decided not to buy shares in the company, despite being bullish on the sector.

The post Why I’m avoiding BP shares! appeared first on The Motley Fool UK.

Should you buy BP shares today?

Before you decide, please take a moment to review this first.

Because my colleague Mark Rogers – The Motley Fool UK’s Director of Investing – has released this special report.

It’s called ‘5 Stocks for Trying to Build Wealth After 50’.

And it’s yours, free.

Of course, the decade ahead looks hazardous. What with inflation recently hitting 40-year highs, a ‘cost of living crisis’ and threat of a new Cold War, knowing where to invest has never been trickier.

And yet, despite the UK stock market recently hitting a new all-time high, Mark and his team think many shares still trade at a substantial discount, offering savvy investors plenty of potential opportunities to strike.

That’s why now could be an ideal time to secure this valuable investment research.

Mark’s ‘Foolish’ analysts have scoured the markets low and high.

This special report reveals 5 of his favourite long-term ‘Buys’.

Please, don’t make any big decisions before seeing them.

setButtonColorDefaults(“#5FA85D”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#43A24A”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#FFFFFF”, ‘color’, ‘#FFFFFF’);

})()

More reading

- BP is one of the cheapest stocks on the FTSE 100. Am I buying?

- Why BP shares are rising today

- Should I buy cheap BP shares today?

- With oil below $85, what’s next for the BP share price?

Mark Tovey has no position in any of the shares mentioned. The Motley Fool UK has no position in any of the shares mentioned. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.