‘Hey, babe, how about I get you an NFT for your birthday? My girlfriend asked after dinner last night. ‘Or I can make NFT of you.’

‘What? You know what an NFT is?

‘Sure I do.’

‘And I thought I was the only web3 nerd around here.’

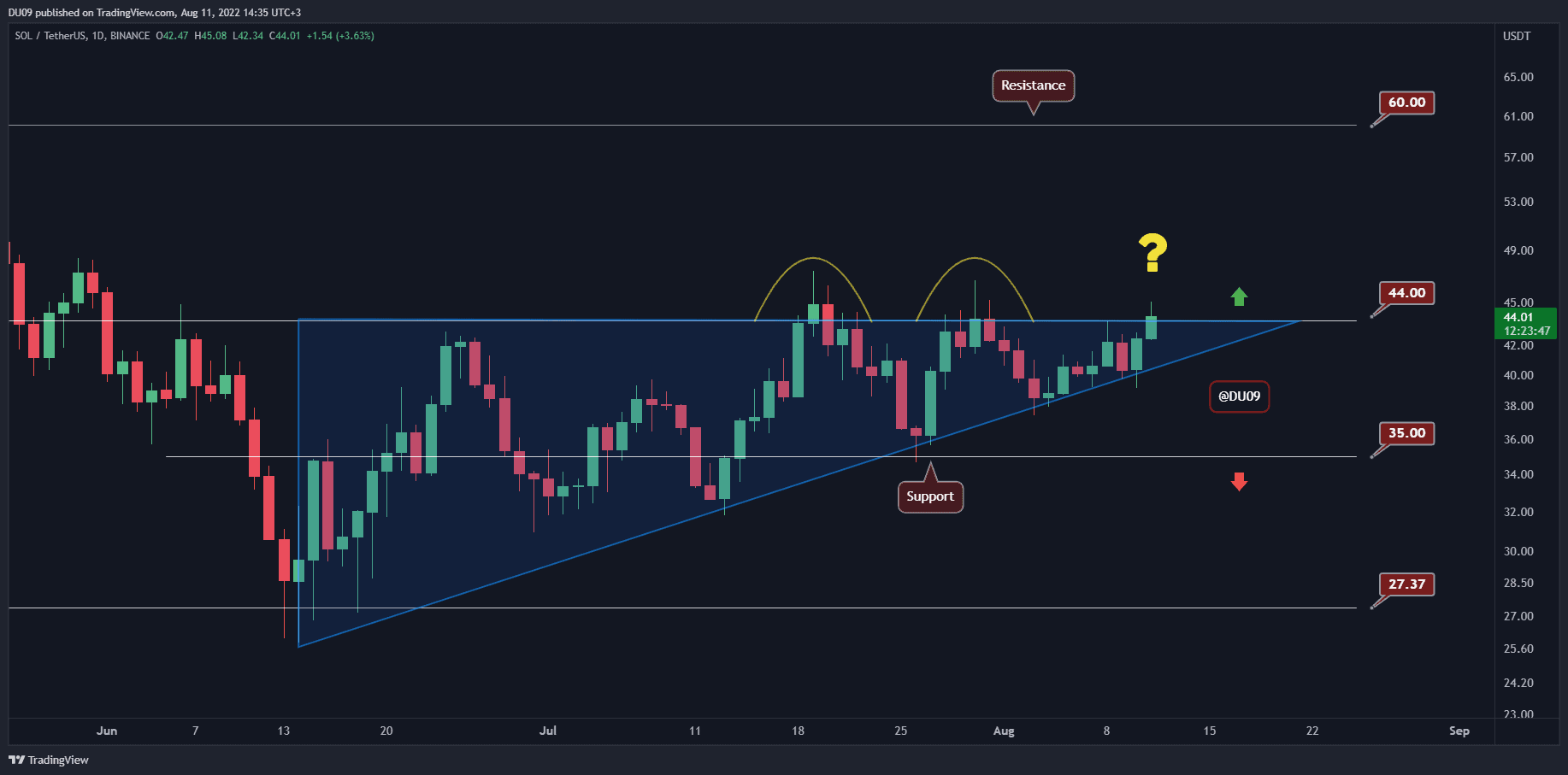

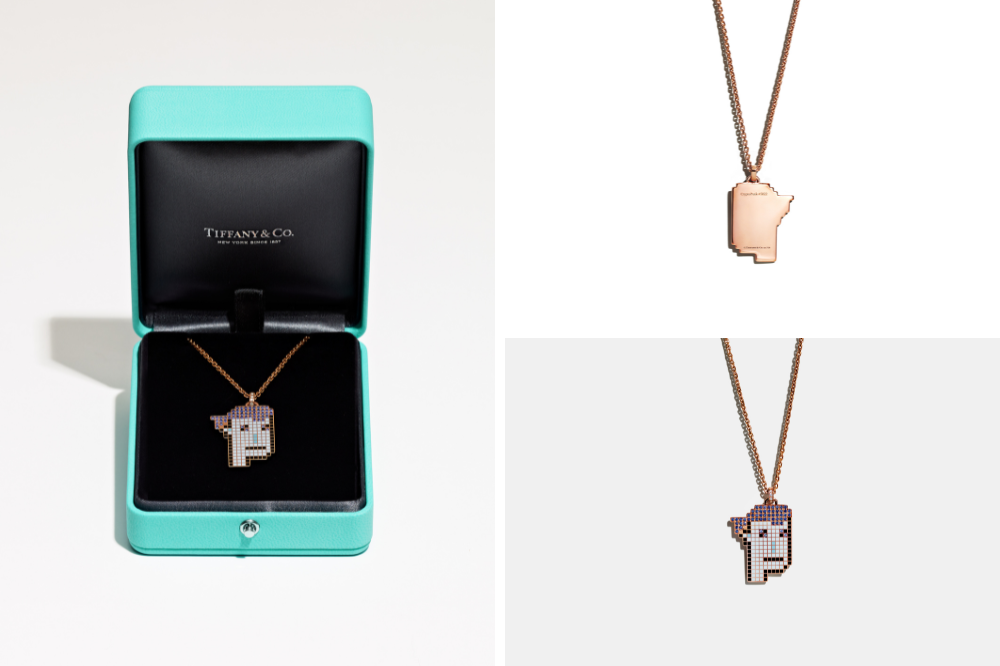

‘No, you’re the only web3 nerd around here, she said, rolling her eyes, ‘but after seeing on the news that Meta expanded their NFT support on Instagram to 100 countries, and that TiffanyAndCo made $12.5M in their NFT sellout, I decided to look up NFTs. After hours of research, I think I’m good.’

‘Alright, explain it to me like I was 10.’

‘Cool, let’s start from the basics.’

What is an NFT

NFTs are digital (or physical) objects you can own. Their ownership is traceable to the blockchain.

NFTs are a way to make digital assets ownable.

NFT stands for Non-fungible token.

Non-fungible means that it’s unique and irreplaceable. For example, you can trade a $10 bill for a similar $10 bill. They’re fungible. But you can’t do that with an NFT. If you exchange it for another, you’ll get something different.

Why do NFTs matter?

NFTs allow anyone to permissionlessly own, issue, store, or trade them.

NFTs make it possible to own an asset without a third-party intermediary.

In the traditional world, you’d depend on the bank or a property registry to maintain the ledger of a property. But NFTs make intermediaries irrelevant.

Before NFTs, we usually made money on big platforms like Facebook, Spotify, etc., through services like ads, publishing, etc. These companies are in control. They take most of the revenues and can decide to ban anyone from their platform. The only way creatives could get to their fans was through these companies. But NFTs help creators connect with their fans.

Also, you don’t own the characters in a traditional video game like Super Mario. You only use them in-game. You can’t sell them, or move them to your wallet. But with NFTs, you can do all these things. You can buy an object, use it in-game, store it in your wallet, plug it into decentralized platforms, trade it with anyone in the world, or even use it as collateral. And you can do all these without needing anyone’s permission.

Let’s further look at how NFTs matter to a creator, a fan, and a collector.

Creators

The point of NFTs to creators is that they allow them to connect to their fans. NFTs also let them sell work for which there might not be a market. For example, before NFTs, if you designed cool stickers or memes, there was no way to sell them. But NFTs helped Chis Torres sell his Nyan Cat meme.

Chris Torres created Nyan Cat (an animated cartoon cat with a Pop-Tart for a torso flying through space and leaving a rainbow trail behind) in 2011 and sold it as an NFT in 2021 for nearly $600k!

Insane right?

According to Torres, crypto art and NFTs offer meme creators an opportunity to earn from their work that would have spread freely online.

“It gives power to the creator. The creator originally owns it, and then they can sell it and directly monetize and have recognition for their work.”

Also, some NFT marketplaces allow artists to gain commission on their NFT each time it exchanges hands. As an artist, you can program your NFT so you’ll earn a commission each time a new buyer buys the NFT.

You can do this in an automated and transparent way.

Fans

NFTs let you appreciate and support your favorite artists. Also, when you buy an NFT, there’s evidence on the blockchain that it belongs to you. You can resell it, hold it, upload it online as your profile picture, or use it in-game. You have the freedom and choice to do whatever you like.

Collectors

NFTs can work as other speculative assets. You can buy them, hold them, and hope the value increases so you can sell them at a profit.

How do NFTs work?

NFTs are great applications for blockchain technology.

A blockchain is a digital ledger that has computational powers. It is decentralized, distributed, secure, and public.

NFTs are parts of different blockchains like Ethereum, Polygon, Binance Smart Chain, and Solana.

The blockchain ensures the permanence of NFTs. This means that when you buy an NFT, that NFT is yours until you give it away.

When you decide to put your work on the blockchain as an NFT, you’ll first have to ‘mint’ it.

Minting is interacting with the smart contract of the blockchain. There are different marketplaces where you can easily mint your NFTs. They let you select other attributes of your NFT. Like the name, price, the types of royalties involved in case of a secondary sale, etc.

To mint an NFT, you must set up a crypto wallet like Metamask. Then you’ll add about $50-$100 worth of ETH or any other token (depending on the blockchain you’re using) to your wallet to cover transaction fees. After these steps, you can head to an NFT marketplace to mint your NFT.

NFT marketplaces

NFT marketplaces allow artists and collectors to buy, create and sell their own NFTs.

Some popular ones include:

- OpenSea

- Foundation

- Rarible

- Mintable.app

- Nifty Gateway

- KnownOrigin

- Fractional.art

- Sorare

- Decentraland

- Async

- Makersplace

- Valuables

- NFTX

- SuperRare

- ZORA

- NIFTEX

- Niftys

- Unicly

- NFTfi

- NBA Top Shot

- Axie Infinity

What can be an NFT

Anything in the world can be an NFT. Anyone can create something unique that someone can own.

Some examples include:

- Art

- Game characters

- Music NFTs

- Books

- Jewelry

- Blog posts

- Tweets

- In-game moments

- Token-gated fitness community

- Token-gated newsletter

The fantastic thing about crypto is it allows people to be creative. We can have all these concepts we never would have thought were possible.

Use cases of NFTs

Some obvious things to do are holding it, selling it, or displaying it to other people. But there are even more innovative things you can do with your NFT like:

- Lending them out,

- Using them as mortgages,

- Borrowing against them,

- Using them as in-game characters.

There are NFT index funds, NFT derivatives, and even fractional ownership of NFTs.

The possibilities of NFTs are endless.

NFTs explained was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.